Recombination

Let There be Light

For almost 400,000 years after the Big Bang, the universe was completely dark. A superheated, highly ionized plasma prevented photons from free streaming. Bare hydrogen and helium nuclei bounced around with free, unbound electrons at universal temperatures approximating those at the surface of the Sun.

As the universe expanded and cooled from over 20,000 K at an age of about 10,000 years toward 3000 K, the ionized, free-rang subatomic particles gradually combined to form neutral atoms. Around a cosmic age 375,000 years, hydrogen nuclei became very efficient at capturing free electrons to form neutral hydrogen atoms. Free roaming electrons that inhibited the travel paths of photons were rapidly incorporated into atomic structures. The fog lifted, and in short order, the universe went from opaque to transparent.

Visible light that escaped into free streams is still detectable today as the cosmic microwave background. The elongation of spacetime as the universe expanded stretched the wavelength of the original light beyond the visible spectrum. It was discovered accidentally by a sensitive microwave receiver in New Jersey that was being used by Bell Labs to explore the transmission of data through microwave channels.

The phase transition from darkness to transparency in the early universe proceeded gradually and then suddenly. The final stages of recombination that allowed uninhibited photon paths took place over 15-20,000 years-a blink of an eye in cosmic time.

Our point in this piece is to highlight a similar, broad phase change on the horizon across the private investment universe.

In fewer than six weeks, the fiscal year will close for many institutional investors. It is one of the few predictions where we will claim a high degree of certainty.

This fiscal year end is significant because it will mark the point at which any investment analysis that utilizes a five-year moving average of returns as an assessment factor will be dropping the results of fiscal 2021 to add fiscal 2026. For investors that use calendar years, the same transition will take place at year end.

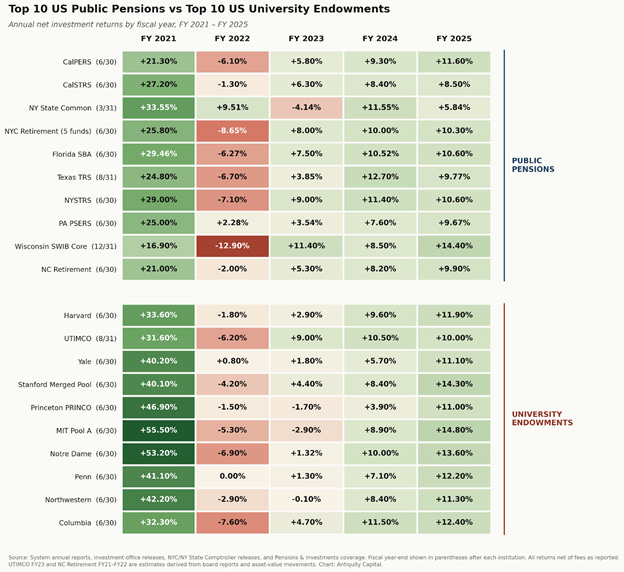

The table below illustrates what will be left behind as the largest pension and endowment funds jettison their 2021 results from five-year performance numbers.

A cursory glance shows clearly that 2021 marked an historic, positive performance anomaly that allowed several of the institutions included above to record the best overall portfolio results in the modern era.

Substantial portions of those results were driven by spectacular mark-ups in venture capital, private equity and public technology holdings.

We have written dozens of times that the tailwind behind these results was the extraordinary degree of monetary ease provided by global central banks in response to the emergence of the Covid 19 virus. It marked the grand finale of a long experiment with near zero interest rates and direct monetization of fixed income instruments through quantitative easing.

In two years, the Federal Reserve added more than $4.5 trillion to its balance sheet, while maintaining a funds rate target of 0.00%-0.25%.

Unprecedented monetary inflation provoked commensurate asset inflation across a wide swath of markets. Hyper-normal returns across the institutional spectrum confirmed the comprehensive effect.

Reported returns from private funds in 2021 have served to enhance the apparent, long-term appeal of the Yale Model of asset allocation. The model emphasizes illiquid, non-public investment conduits over public securities and has been adopted across the institutional realm since its introduction in the mid-1980s.

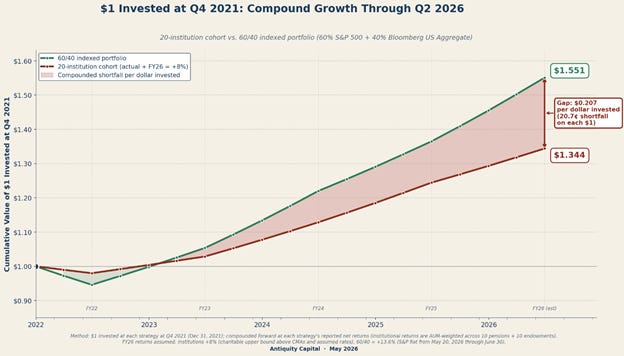

The chart below shows the cumulative, trailing five year returns for two distinct asset allocation approaches. To fashion it, we replaced the departing record from 2021 with an estimated institutional return of 8% for fiscal 2026. The 8% number represents about a percent and a half of author’s generosity, given that most preliminary estimates are between 6% and 7% for institutional portfolios for fiscal 2026.

Actual results from the 20 institutions shown in the first table are used as a compounding factor for the red line. The green line is the final, compounded value of the same dollar invested 5 years ago in the dreaded 60/40 passive model. Both are indexed to one at the outset.

Even with the less liquid institutional portfolios outperforming during the first portion of 2022, the current results are skewed heavily in favor of the least imaginative, low-cost allocation to public equity and fixed income indices. The red shaded area shows the degree to which the best and brightest have fallen behind.

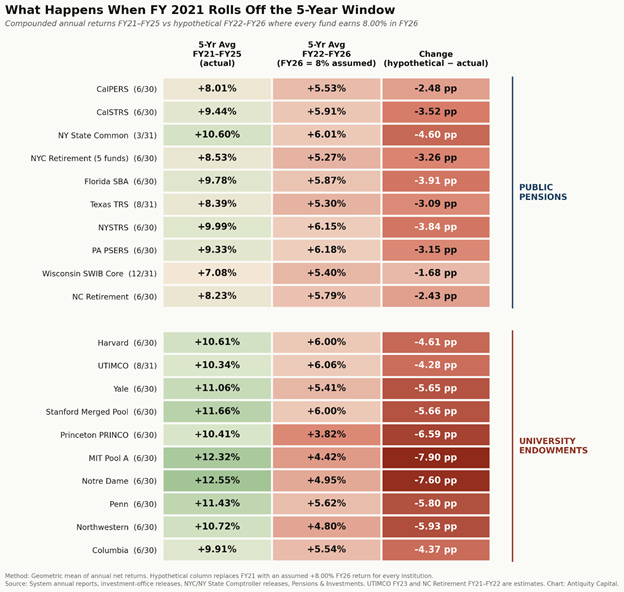

The underperformance metrics on an institution-by-institution basis are displayed in the table below:

The column on the right displays the level of decline in average annual returns that will be the result of replacing 2021 with the 8% assumption for the current year. The changes are sufficiently abrupt and severe to constitute a change of phase in the investing world.

The trailing 5-year number shown in the middle column is substantially below the passive 60/40 mix for every institution shown. The underperformance vs. equity index funds is even more pronounced.

Included in the institutional results are private fund values as reported by managers, with no consideration of the possibility that some of the model-based valuations might be overstated.

The institutions listed here are among the most highly sophisticated, well-advised investors in the world. Each has access to elite consultants, academic theorists and the most comprehensive and exclusive research from investment banks and independent sources.

The practical consequences of forgone opportunities and results that fall below actuarial assumptions and spending need could be severe in certain cases. Trustees, board members and others with fiduciary duties that require constant monitoring and questioning to fulfill their oversight responsibilities are largely unaware of the statistical transition that is taking place.

Thus far in the process of retreat from the exuberance of 2021, general concerns have been centered around retail investors’ issues with illiquid private credit funds. In our previous post (Entanglement), we argued that attention was about to shift toward traditional, closed-end private equity vehicles, which are in aggregate far larger than the world of retail focused BDCs.

We anticipate a period ahead where the general merits and assumptions surrounding private markets will become the focus of more open and widespread debate. Tailwinds from the anomalies of 2021 are dying out, and a cooler and more transparent epoch is on the horizon.

For additional details or comments, please contact Michael@Antiquitycapital.com

Interesting how endowments outperform pension plans. How is their portfolio composition different? More aggressive?